Research from Savills World Research team suggests that, following a relatively resilient 12 month period, logistics and operational residential assets will continue to come top of investors’ wish lists throughout 2021.

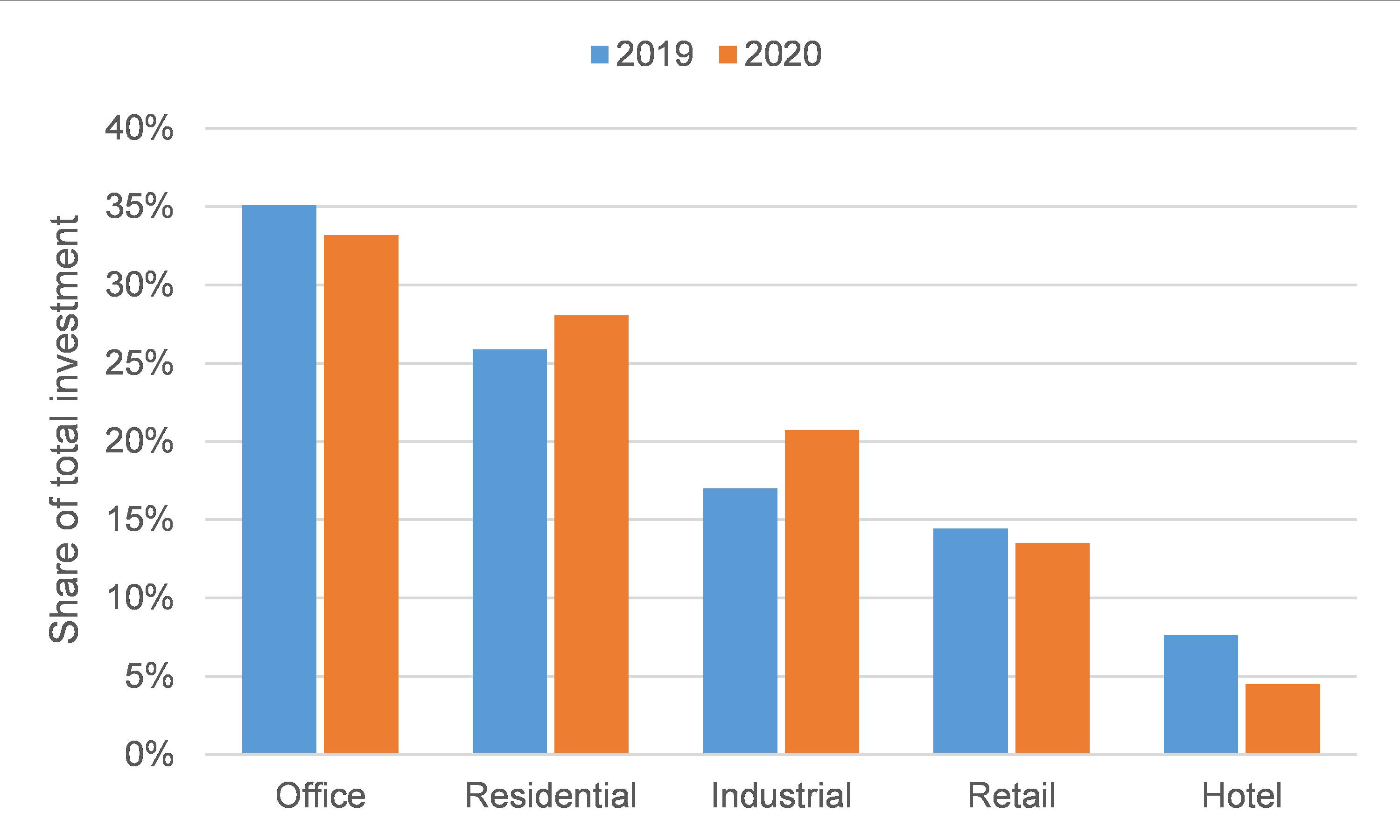

Share of total investment chart click here

{kind=link}

In an update to its global research programme, Impacts, in the 12 months to November 2020, the international real estate advisor says that although global investment volumes into real estate were down by 28% compared to the same period in 2019, not all sectors felt this equally. The industrial and residential sectors saw more modest falls in volumes, gaining market share to capture 21% and 28% of total investment, respectively (see chart).

Source: Savills Research using RCA, data covers 12 months to November of stated year

Savills goes on to suggest that, in spite of the ongoing uncertainty brought about by Covid-19, the long term appeal of the real estate sector and the number of funds targeting it has continued to rise. Data from Preqin indicates that as of the beginning of Q4 2020, there were over 1,000 funds in market – more than double the number in January 2016. Funds are now targeting almost $300bn of investments, with investor momentum likely to continue into 2021.

Rasheed Hassan, Head of Savills cross-border investment team, commented: “Our investment forecasts suggest that, despite the adverse knock-on effects from Covid-19 on real estate, there is still a lot of dry powder waiting to target real estate once the dust settles. While logistics and residential will continue to be top picks over the course of the next 12 months, alongside offices, we anticipate activity will return to most sectors of the market as the vaccine becomes rolled out widely across the globe.”

Savills sector themes for global real estate investment in 2021:

- The pandemic accelerated a shift to online retail and flexible working patterns. In 2021 logistics is expected to be the major beneficiary, but the challenge for investors will be finding stock.

- The office sector is forecast to remain the largest sector and the core investment of choice. Emphasis will be placed on lower risk assets with stable income characteristics in the best locations.

- Residential may attract a growing share of global investment, supported by strong underlying fundamentals and cross border investors growing and consolidating portfolios.

- Senior housing and healthcare are operational asset classes with long-term income potential. Ageing populations and emphasis on health and wellbeing is expected to support expansion.

- Datacentres are a rising alternative sector and offer opportunity for portfolio diversification. Yields are attractive and pent up demand is likely to fuel growth in 2021, but barriers to entry are high.

- 2020 brought life sciences to the fore. A big increase in capital raising is forecast to spur real estate investment opportunities in a sector resilient to changes in working habits.

- Despite the challenges of 2020, the importance of environmental, social and governance (ESG) credentials for investors will continue to grow, particularly as more governments across the globe make ‘climate emergency’ declarations and commit to net zero carbon

Sophie Chick, Director in the World Research team, added: “With ESG so high on investors’ agendas, the real estate industry has a real opportunity to lead the way and make a significant difference when it comes to creating a sustainable future. To support government commitments to meeting net zero carbon, new investment into green technology, energy and much more has been announced but also an increasing amount of regulation.”